QUICK SUMMARY

Behind every generic unified communications market statistic is a complex engineering reality. As the industry shifts from basic cloud adoption to advanced API convergence and Agentic AI, telecom architects and product leaders need more than high-level financial forecasts.

This blog decodes the conflicting UCaaS market sizes, regional architectural demands, WebRTC failure modes, and the convergence of UCaaS, CCaaS, and CPaaS to help team leaders map a highly scalable, resilient 2026 telecom roadmap.

Knowing that the “unified communications market is rapidly growing” is completely useless to an engineer mapping out a product roadmap. A generic growth chart won’t help you decide whether to invest in edge WebRTC media servers, or if you need to overhaul your Session Border Controller (SBC) architecture to support Bring Your Own Carrier (BYOC) models.

The unified communications industry has officially moved past the era of basic cloud adoption. The massive PSTN copper shutdowns in late 2025 forced the final holdouts into the cloud, meaning the next decade of growth will rely on complex API convergence, stringent data sovereignty, and advanced AI workloads that demand flawless real-time communications (RTC) pipelines.

Let’s look at the actual engineering trends and technical realities driving the UCaaS market in 2026.

What Is the Real Unified Communications Market Size?

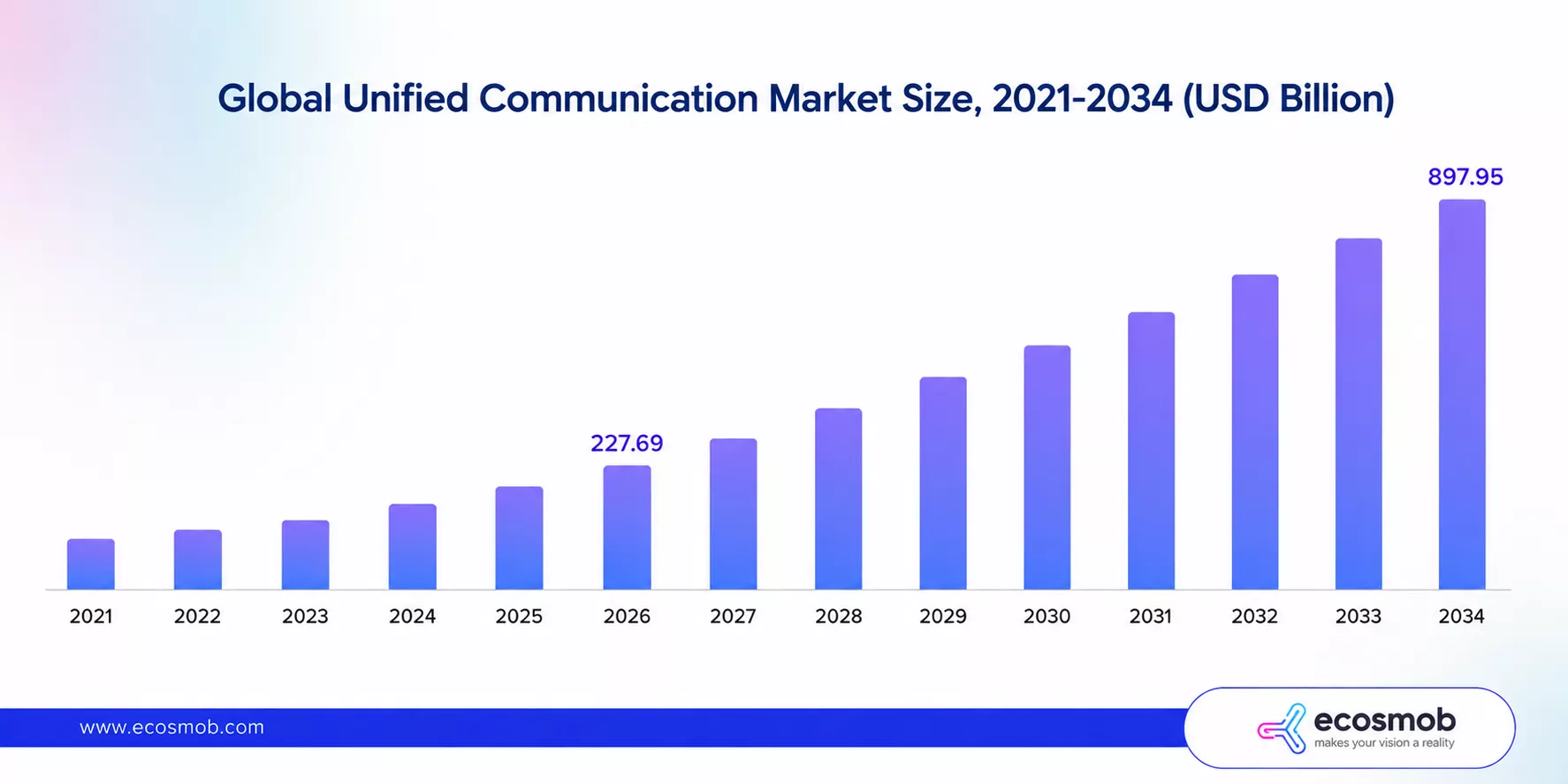

If you read three different market reports, you will see three wildly different valuations for the UCaaS industry. This lack of transparent number reconciliation causes massive confusion for operators planning their CAPEX and OPEX budgets.

The Broad Unified Communications Market is valued at $227.69 billion in 2026 and projected to hit $897.95 billion by 2034 (an 18.71% CAGR).

- This massive figure includes legacy on-premise hardware, legacy PBX maintenance contracts, raw SIP trunking, and physical endpoints. It is the entire pie.

The Unified Communication as a Service (UCaaS) Market is valued at $78.15 billion in 2026, reaching $276.9 billion by 2034 (a 17.10% CAGR).

- This is the pure cloud-hosted, software-driven layer. It strips out the legacy hardware and focuses entirely on subscription-based cloud delivery.

Despite the heavy marketing focus on video and chat, cloud telephony still accounts for roughly 37% of UCaaS component revenue in 2026. Voice routing remains the critical, unforgiving backbone of the industry.

Where is the Fastest Unified Communications Growth Happening in 2026?

Where is the Fastest Unified Communications Growth Happening in 2026?

Generic reports tell you that North America dominates the UCaaS market (holding roughly 38% of the global share). But North American growth is stabilizing as enterprises focus on consolidating their existing stacks on AWS, Azure, or Google Cloud. The most aggressive architectural challenges (and revenue opportunities) are happening at the country level across the globe.

- India (24% CAGR): Growth here is not just about volume; it is about architecture. Tier-1 manufacturers and massive BPOs are aggressively moving to BYOC (Bring Your Own Carrier) models to escape vendor lock-in, demanding highly scalable telemetry and open SIP standards from their UCaaS providers.

- Germany (18% CAGR): German enterprises are adopting UCaaS but strictly demanding on-premise SBCs and localized media servers to ensure GDPR data-sovereignty compliance in UCaaS and topology hiding.

- Japan & Vietnam: These regions are pioneering the intersection of 5G and Edge Computing in UC. By anchoring media servers closer to the edge, telecom operators here are reducing video latency more compared to centralized US-based cloud routing.

- Latin America: Generating an estimated $5.88 billion in 2026, UCaaS growth in Latin America is fueled by nearshoring IT and support services. This creates a massive demand for robust, low-latency cross-border SIP trunks connecting LATAM agents seamlessly to US-based CCaaS platforms.

As you can see, scaling a UCaaS platform globally isn’t about buying more cloud space; it requires edge media servers, localized NAT traversal, and secure SBC deployments to comply with regional data laws. If your audio quality degrades the moment a call crosses an ocean, your routing architecture needs an overhaul.

Audit Your UCaaS Architecture with Ecosmob!

Tired of rigid, off-the-shelf UCaaS platforms throttling your growth?

The Top Verticals Reshaping the Unified Communications Industry

Different industries require completely different underlying infrastructure. The unified communications market leaders are no longer selling one-size-fits-all platforms; they are engineering vertical-specific RTC pipelines.

BFSI (Banking & Finance)

Holding the largest revenue share (22.37% in 2025), banks aren’t just buying generic UCaaS. They require bespoke platforms integrated with on-premise SBCs for strict topology hiding. Every packet must enforce encryption, and routing engines must dynamically support STIR/SHAKEN call authentication protocols to mitigate spoofing and comply with international financial auditing regulations.

Healthcare

UCaaS in healthcare is the fastest-growing (13.90% in 2026) vertical and has moved beyond basic telehealth video. The technical demand now is bidirectional SMART on FHIR integrations, embedding the UCaaS dialer directly into EHR systems (like Epic or Cerner) so clinical data writes back to patient files in real-time during a call.

Manufacturing (19.88% CAGR)

The modern factory relies on “Unified Namespaces” and IoT edge gateways. Engineers are using CPaaS APIs to integrate factory floor sensors directly into the UC environment, meaning an overheating machine can instantly trigger an automated SIP voice call or SMS to the floor manager’s mobile device.

Which AI Technologies Are Driving Unified Communications Growth?

Agentic AI workflows, real-time speaker diarization, and live conversational intelligence are dominating UCaaS trends in 2026. However, these powerful LLM-driven features break down completely when your underlying WebRTC media pipeline suffers from packet loss or jitter.

Every vendor claims to have “AI in UC.” But when we look at unified communications trends, there is a massive divide between marketing claims and engineering reality.

- Conversational Cost Reduction: According to Gartner, conversational AI deployments within contact centers will reduce agent labor costs by $80 billion by 2026.

- Agentic AI Routing: By the end of 2026, inbound routing will be dominated by Agentic AI. Agentic AI is an autonomous system that executes multi-step workflows (e.g., updating Salesforce, sending an email, and rescheduling a SIP call) during a live session.

- Speaker Diarization: Real-time translation and transcription APIs (like OpenAI Whisper) are seeing massive adoption. They’re enabling meeting summarization with strict speaker diarization (the ability of the AI to accurately identify who said what in a crowded room), and live sentiment analysis.

Where AI Breaks in UCaaS

AI features break down instantly under poor WebRTC conditions. Generative AI models and transcription engines process audio streams. If your network suffers from high packet loss, network jitter, or codec mismatch (e.g., failing to transcode G.711 to Opus cleanly), the AI receives mangled audio.

When an AI transcription engine gets hit with packet loss, it doesn’t just pause; it hallucinates data. If you want to deploy advanced AI features, you must first perfect your underlying media routing, jitter buffers, and Quality of Service (QoS) tagging.

You cannot run next-generation Agentic AI and live transcription on a fragile VoIP network. If your AI meeting summaries are inaccurate or hallucinating, the problem is likely your WebRTC media routing, not the LLM.

Let Our WebRTC Engineers Help Fix Your Media Pipelines!

The Convergence of UCaaS, CCaaS, and CPaaS

Historically, enterprises bought their telecom stack in silos. They licensed UCaaS for internal employee calling, CCaaS for their external customer service agents, and CPaaS (APIs) to send automated SMS alerts from their mobile apps. Managing these three fragmented, isolated telecom stacks is an architectural and financial nightmare.

Because of this, the lines between unified communications (internal), contact centers (external), and programmable communications (embedded) have entirely collapsed.

Gartner says by 2028, over 90% of enterprises will rely on cloud platforms for their core telephony, and they expect all of these functions to live under one roof.

The future of unified communications is single-vendor convergence. But architecturally, building this unified API layer is incredibly complex.

To achieve convergence, vendors are using CPaaS APIs (like Twilio or Sinch) as the foundational “glue.” This allows businesses to inject video directly into their proprietary mobile apps, while simultaneously overlaying CCaaS omnichannel routing logic directly on top of the UCaaS employee telephony base (like MS Teams or Zoom).

This requires a masterfully engineered SBC architecture to handle the signaling translations between disparate protocols without introducing latency.

UCaaS vs. CCaaS vs. CPaaS in 2026

| Telecom Layer | Primary Function | The 2026 Engineering Goal |

| UCaaS (Internal) | PBX calling, team messaging, and video meetings. | Consolidating the employee tech stack and enabling BYOC (Bring Your Own Carrier) for lower SIP trunking costs. |

| CCaaS (External) | Omnichannel customer routing, IVR, queue management. | Embedding Agentic AI to autonomously resolve tier-1 support tickets before they reach a human agent. |

| CPaaS (Embedded) | APIs for SMS, voice, and video. | Serving as the “glue” that injects real-time communication directly into proprietary mobile apps and ERPs. |

Struggling to unify your SIP routing, CCaaS, and CPaaS APIs?

The UCaaS Buyer’s Playbook: Build, Buy, or Migrate?

Looking at these UCaaS trends and massive growth projections, telecom CTOs and enterprise architects are left with a critical decision. Do you license an off-the-shelf product, or do you build your own infrastructure? Here is the actual engineering playbook:

- When to Buy: If you are a standard SMB with generic workflows, standard office hours, and no legacy proprietary software to integrate with. License an off-the-shelf white-label platform and focus on your core business.

- When to Build (Custom UCaaS): You must build custom if you require deep API integration into legacy ERPs, specific codec control for low-bandwidth environments, or BYOC (Bring Your Own Carrier) flexibility. Building your own FreeSWITCH or Kamailio-based core ensures you own your media paths, avoid crippling bandwidth egress fee traps, and completely escape vendor lock-in.

- When to Migrate: It is time to migrate off a white-label vendor when per-user licensing costs outpace the cost of hosting your own cloud infrastructure, or when your current provider’s closed architecture exposes you to uncontrollable toll-fraud risks.

The era of simply “moving to the cloud” is over. As the unified communications market surges, the winners will not be the companies that buy the most off-the-shelf licenses; they will be the operators who engineer the most resilient, AI-ready SIP architectures.

Whether you are navigating strict data sovereignty laws in Germany, engineering low-latency WebRTC pipelines in Japan, or attempting the complex API convergence of UCaaS and CCaaS, your underlying telecom infrastructure dictates your ceiling.

You can either let vendor lock-in dictate your product roadmap, or you can take control of your media paths, customize your SBCs, and build a unified communications platform that actually scales.

Ready to build, scale, and optimize your unified communications platform?

Consult Ecosmob’s experienced UCaaS architects today!

FAQs

What is driving the massive unified communications growth in 2026?

UCaaS growth is primarily spearheaded by the convergence of UCaaS, CCaaS, and CPaaS, allowing enterprises to manage internal collaboration and external customer experience on a single unified API layer. Additionally, the mandatory transition away from legacy PSTN networks is forcing remaining on-premise deployments into the cloud.

What are the top unified communications trends right now?

The dominant trends include the integration of Agentic AI for live call workflows, strict speaker diarization for meeting summarization, the rise of Bring Your Own Carrier (BYOC) models, and a heavy engineering focus on edge computing to reduce WebRTC latency in regions like Japan and LATAM.

Why do unified communications market size estimates vary so much?

Estimates vary based on the scope of the report. The broader unified communications market (approaching $227 billion) includes legacy hardware, on-premise PBX systems, and SIP trunking. Reports focusing strictly on the UCaaS market (around $78 billion) measure only the software-driven, cloud-hosted subscription revenue.

How is AI impacting the future of unified communications?

AI is shifting from simple post-call analytics to real-time, autonomous actions. However, the effectiveness of AI features (like live translation and sentiment analysis) is entirely dependent on the quality of the underlying WebRTC audio stream. Poor network QoS and packet loss will cause AI models to fail or hallucinate.

Why do AI transcription and meeting summaries fail in unified communications?

AI transcription and meeting summarization tools fail primarily due to poor WebRTC network conditions, not the AI models themselves. When a VoIP network experiences high packet loss, jitter, or codec mismatches, the audio stream is mangled. The AI engine receives broken audio and is forced to hallucinate or skip data, resulting in inaccurate summaries.